Welcome to the second instalment

Welcome to part two of our special five-part series, which delves into the 10 factors you need to consider, as a business owner, when planning your financial future.

In the initial instalment of this series, we discussed superannuation and diversification; today we look at the important issue of risk management and explore the various funding options available which can help support the growth of your business.

3. Risk Management

Risk management and appropriate insurance coverage are essential components of a well-structured financial plan as they work to protect you and your business against unexpected events that could jeopardise your business and overall financial wellbeing.

Unfortunately, whilst risk management is something every small business owner needs to consider, it often falls to the bottom of the to-do list as identifying and mitigating every applicable risk from natural disasters through to reputation, operational or financial risks can be an overwhelmingly daunting task.

However, insurance undoubtedly plays an integral role in helping to safeguard everything you have worked hard to achieve across both your personal life and the life of your business, therefore knowing what options are available to you is essential.

Personal insurance options

Personal insurance options include:

Life Insurance

This pays a lump sum when you die or are diagnosed with a terminal illness. This cover is important if you have loved ones who depend on you, especially if you have a mortgage or other debts.

Total and Permanent Disability Insurance

A lump sum payment is paid in the event you become totally and permanently disabled and are unlikely to return to work. This money can be used to pay for rehabilitation costs, living expenses, mortgage repayments and more.

Critical Illness or Trauma Insurance

A lump sum is paid for serious illnesses or injuries (such as cancer, heart attack, coronary bypass or stroke) to provide financial support while you recover.

Income Protection Insurance

This cover protects one of your biggest assets — your ability to earn an income. It pays a percentage of your income on a regular basis if you are unable to work due to sickness or injury.

There is a plethora of business insurances that can help you protect your business, customers and income and it is important to understand the different types of insurances available so you can select the ones best suited to your circumstances.

For example, there are insurances are that legally required such as workers’ compensation, public liability and compulsory third-party (‘CTP’). In addition, there are optional protection policies such as professional indemnity, technology and cybercrime, as well as various stock, products and asset insurances.

Debt getting you down?

Many business owners take on debt to launch their businesses. Depending on how well the business then performs, some might struggle with loan repayments as it takes time to work up to a healthy income to cover your expenses and grow. If you’re struggling to pay your debts, it’s imperative to talk to a financial adviser about consolidating your debt and getting you back on the right financial track.

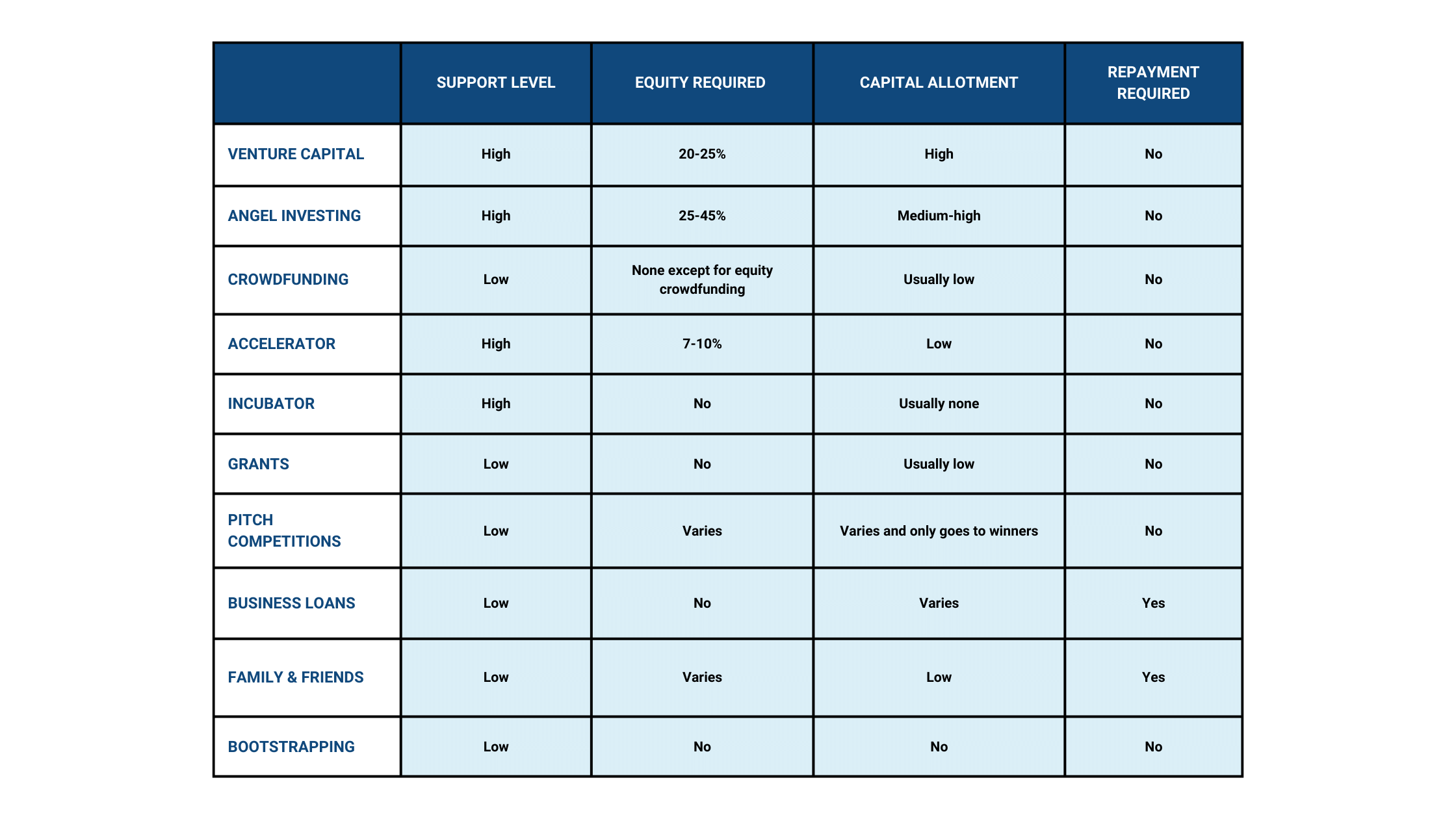

4. Funding Options

Choosing the right funding option for your business can be a catalyst for growth, but with so many ways to finance your business, it’s important to consider your business’s financial needs, potential for growth and expansion goals when deciding which funding option best suits your unique needs.

As a business owner, it’s important to evaluate the various funding options available and their pros and cons as one of the most crucial decisions to make is choosing the right funding option for you.

Listed below is a range of funding options available:

Venture capital (VC)

This is a form of private equity and financing that investors provide that are perceived to have long-term growth potential. VC funding tends to come from affluent investors and various financial institutions.

Angel investing

An angel investor provides initial seed money for startup businesses, usually in exchange for ownership equity in the company. The investor’s involvement may be a one-time infusion of seed money or an ongoing injection of cash to get a product to market. Angel investors usually acquire a return only if and when the business takes off.

Crowdfunding

This is the use of small amounts of capital from a large number of individuals. It leverages the power of mass reach via social media and websites to bring investors and entrepreneurs together whilst simultaneously expanding the pool of potential investors beyond the traditional parameters of owners, relatives and venture capitalists.

Accelerators (i.e. seed accelerators)

These are fixed-term, cohort-based programs, that include mentorship and educational components and culminate in a public pitch event or demo day.

Incubator

These usually work on a fee-basis as opposed to taking an equity stake in a business. This is the case when institutions such as universities or government organisations fund incubators. Alternatively, profit-driven incubators will look to gain equity in the company in exchange for their services or seed capital.

Business grants

A business grant is an award, usually financial, given by one entity (typically a company, foundation, or government) to a company to facilitate a goal or incentivise performance. Whilst they do not have to be paid back, the funds must be used in accordance with the terms of the grant.

Pitch competitions

Here, a number of business owners give a verbal presentation about their company. Depending on the type and scale of the competition, prizes range from hundreds of dollars to millions.

Business loans

This is an arrangement whereby a business is provided funding, usually by a financial institution such as a bank to finance a variety of purposes, such as daily expenses, new equipment, hiring employees, expanding operations or consolidating existing business debt.

Friends & family

This is simply money borrowed from either family or friends in order to help finance a startup or growing business.

Individual investors

Here an individual puts money into a business for a financial return. The main goal of any investor is to minimize risk and maximize return.

Bootstrapping

Here a business owner is said to be bootstrapping when they attempt to found and build a company from personal finances or the operating revenues of the company itself without relying on any external funding sources.

Here at Profile Financial Services we can help to minimise your risk, as well as help guide you on the path to business growth. Simply contact our team to find out how.

Stay tuned for part three, where will uncover why cash flow is crucial, the value of proactive tax management, plus we’ll share some tips for creating a consistent cash flow!